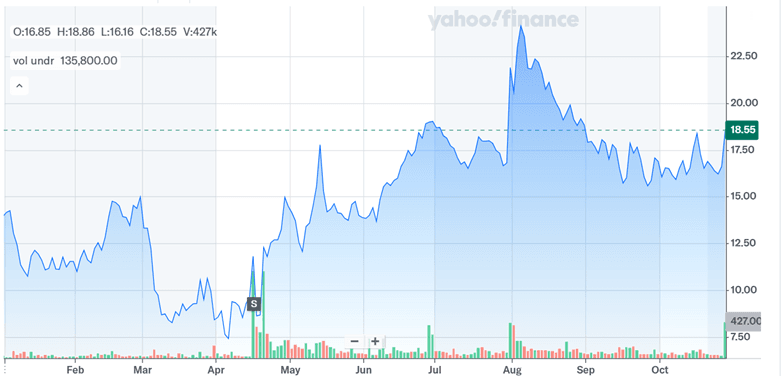

Forge Global Holdings (NYSE:FRGE) saw its stock spike after reports emerged that the company is exploring a potential sale. According to a Financial Times report, Forge has enlisted Financial Technology Partners to help evaluate strategic alternatives amid a sharp drop in market capitalization and mounting liquidity concerns. The news comes on the heels of a 45% decline in Forge’s market value between August 5 and October 24, 2025, which now sits at just $226 million. The company’s cash and short-term investments have also deteriorated rapidly, falling from $193 million at the end of 2022 to just $80.7 million by June 30, 2025. While these financial headwinds have constrained Forge’s ability to issue equity or raise capital, the company continues to push ahead with new product rollouts, including its next-generation trading marketplace and retail-accessible funds. Still, the sale process appears to be a direct response to a challenging macro and microeconomic backdrop, with interest from potential suitors such as Wall Street firms looking to diversify away from public market reliance.

Plummeting Valuation Has Severely Constrained Strategic Options

Forge Global’s stock price collapse has been matched by a steep deterioration in its valuation multiples, both on a forward and trailing basis. As of October 27, 2025, Forge trades at a trailing price-to-sales ratio (P/S) of 2.78x and a trailing EV/revenue multiple of 1.99x. More concerning is the company’s negative enterprise value-to-EBITDA ratio of (2.96x) and EV/EBIT of (2.86x), indicating that the company is generating negative earnings before interest, taxes, depreciation, and amortization. Forward-looking multiples paint an equally bleak picture, with the company trading at a forward EV/EBITDA of (11.41x) and EV/EBIT of (3.92x). Such deeply negative profitability ratios indicate that Forge is operating under structural inefficiencies that cannot be easily remedied without drastic cost realignments or external capital infusions. This steep discount relative to the firm’s 2021 SPAC valuation of $2 billion reflects not only a reassessment of its business model, but also investors’ eroding confidence in the platform’s long-term scalability. With Forge’s equity value now a fraction of its peak, the company has few levers left outside of strategic alternatives. Issuing new equity is largely off the table, and raising debt capital would come at punitive terms given its deteriorating financial profile. In this context, exploring a sale emerges less as a strategic opportunity and more as a defensive necessity.

Deteriorating Liquidity Profile Heightens Urgency For A Sale

Forge’s cash position has eroded substantially over the past two years, shrinking from $193 million at year-end 2022 to just $80.7 million as of June 30, 2025. While the company has made progress in reducing its adjusted EBITDA losses—reporting a $5.4 million loss in Q2 2025, down from $8.9 million in Q1—the business remains firmly in the red. Cash burn from operating activities was $7.8 million in the second quarter alone, compared to $12.8 million in Q1, signaling some improvement in working capital efficiency. Nevertheless, Forge's runway remains tight, particularly considering its limited access to external financing. Compounding the liquidity issue is the company’s increasing reliance on transaction-based revenue, which remains volatile and difficult to forecast amid broader macroeconomic uncertainties. Despite growth in trading volume and take rates, recurring revenue streams have yet to reach material scale. Liquidity constraints are also highlighted by Forge’s modest buyback activity, with only 315,000 shares repurchased at $13.15 on average during the quarter—suggesting limited firepower for capital deployment. With its current pace of spending and revenue concentration, Forge faces a real risk of liquidity stress by mid-2026 absent a significant capital injection. Thus, the urgency to find a strategic buyer is underpinned not only by valuation pressures but also by a rapidly narrowing financial runway.

Public Market Sentiment Remains Tepid Despite Platform Innovations

Despite notable advancements in product development, investor sentiment toward Forge Global remains cautious. The company recently launched its next-generation trading platform, which introduces automated negotiation features and enhanced API integrations. Forge has also broadened its index-based pricing offering, “Forge Price,” now covering nearly 200 private companies, and has struck data-sharing agreements with ICE and Fortune Media. Additionally, the acquisition of Accuidity is enabling Forge to roll out new registered funds aimed at retail and non-accredited investors. Yet these product milestones have not translated into a sustained re-rating of the stock. Market participants remain skeptical, as reflected in persistently negative valuation multiples and subdued trading liquidity in the stock. The seasonal nature of transaction volumes—typically slower in Q3—also limits near-term visibility into growth acceleration. While Forge aims to reach adjusted EBITDA breakeven by 2026, its forward EV/EBITDA multiple of (11.41x) suggests investors are not yet pricing in that optimism. Furthermore, the company's market position in the fragmented secondary trading ecosystem for private shares continues to face pressure from both legacy broker-dealers and fintech entrants. Forge's long-term growth narrative hinges on expanding retail access to private markets and integrating custody, trading, and data services into a seamless offering. However, until those initiatives yield durable recurring revenues and margin expansion, the market is likely to remain on the sidelines.

Institutional Demand & IPO Tailwinds Could Support Short-Term Upside

One of the few bright spots in Forge Global’s current situation is the recent resurgence in U.S. IPO activity, which has historically been a strong catalyst for its trading volumes. In the first half of 2025, over 174 companies went public, raising $31 billion—the strongest showing since 2021. Notably, Forge’s Q2 trading volume of $756 million surpassed the total volume for the entire year of 2024, reflecting a material uptick in platform engagement. The median bid-ask spread on its platform narrowed to just 3%—a level not seen since early 2021—indicating stronger price discovery and improving liquidity conditions. Buy-side interest is also increasing, with institutional buyers accounting for 64% of all platform indications of interest in June. In addition, Forge’s AI-themed private market basket has returned 63.1% year-to-date, significantly outperforming public benchmarks like the AIQ ETF, further validating investor interest in high-growth private names. These positive dynamics suggest that Forge is not lacking demand-side traction. Instead, the challenge lies in translating that demand into sustained revenue and profitability. If broader IPO activity continues to accelerate, Forge could benefit from increased commission revenues and fund inflows, particularly through its new index-tracking and diversified access vehicles. However, such upside remains contingent on the macro backdrop, market sentiment, and Forge’s ability to convert interest into closed transactions.

Final Thoughts

Source: Yahoo Finance

Forge Global’s recent stock surge reflects growing market interest following reports of a potential sale, but the underlying fundamentals remain strained. The company’s market cap has cratered to $226 million—down 45% in under three months—while cash reserves have dwindled to just $80.7 million. Despite executing well on product innovation and reducing adjusted EBITDA losses, Forge continues to operate at a loss with negative earnings and declining operating cash flow. LTM valuation multiples underscore this stress: the company trades at a price-to-sales ratio of 2.78x and a TEV/revenue of 1.99x, but deeply negative TEV/EBITDA and TEV/EBIT ratios of (2.96x) and (2.86x), respectively. While a stronger IPO environment and rising institutional activity offer some tactical support, Forge’s structural issues—volatile revenues, limited recurring income, and shrinking liquidity—make the case for a strategic sale increasingly compelling. Investors and acquirers alike will need to weigh short-term momentum against long-term scalability when assessing Forge’s potential.