Intellia Therapeutics (NASDAQ:NTLA) just had one of those gut-punch moments no biotech ever wants to face. The small-cap gene-editing company saw its stock tumble more than 20% after revealing that a patient had died during a clinical trial of its experimental therapy, nex-z, designed to treat transthyretin amyloidosis (ATTR). The patient, an 80-year-old man with heart disease, suffered serious liver complications a few weeks after receiving the dose. That single event led the FDA to place both of Intellia’s Phase III trials on hold, freezing progress while regulators dig into what happened. For a company once viewed as one of the frontrunners in CRISPR-based medicine, the tragedy has quickly turned into a defining test. Investors, analysts, and even rival biotech watchers are now focused on one question—how will Intellia navigate safety concerns, regain investor trust, and protect the future of its small-cap pipeline after such a painful setback?

Safety Profile & Clinical Hold Impact

The biggest immediate influence on investor sentiment revolves around the safety concerns and resulting clinical hold imposed by the FDA on both nex-z trials. Intellia’s CEO, John Leonard, acknowledged that while only less than 1% of enrolled patients had experienced Grade 4 liver enzyme elevations, the fatality forced an automatic protocol pause. The company halted patient dosing and screening not only in the MAGNITUDE trial for ATTR-cardiomyopathy but also in MAGNITUDE-2 for ATTR-polyneuropathy as a precaution. Intellia is now working with the FDA and global regulators to determine the root cause, which will dictate how quickly—or whether—the studies can resume. In biotech, particularly for small-cap players like Intellia, safety setbacks can drastically alter valuation trajectories. Even a temporary hold delays revenue timelines, regulatory submissions, and potential partnership negotiations. Historically, prolonged clinical holds can weigh heavily on both investor trust and cash flows. However, Intellia’s leadership insists it remains committed to the program, pointing to a strong dataset where the vast majority of over 650 patients experienced no major adverse events. Until clarity emerges on whether the liver issue was drug-related or driven by the patient’s age and comorbidities, investors are likely to remain cautious, pricing in regulatory risk and extended development timelines.

Lonvo-Z’s Progress & Its Role As A Diversification Hedge

While nex-z dominates headlines, Intellia’s second key program, lonvo-z, may act as a partial cushion for investor sentiment. Lonvo-z, designed to treat hereditary angioedema (HAE), uses the same lipid nanoparticle delivery system as nex-z but targets a completely different gene. The company recently completed enrollment in its Phase III HAELO trial and expects top-line results by mid-2026, followed by a potential U.S. launch in 2027. During the recent call, Leonard emphasized that lonvo-z’s clinical experience has been distinct from nex-z, with no severe liver enzyme elevations reported. Investors see this distinction as critical because it suggests that any safety signal may not be platform-wide but program-specific. Still, perception risk lingers: negative sentiment toward CRISPR safety could spill over into other pipeline assets. For a small-cap like Intellia, which relies heavily on pipeline promise, diversification across distinct indications helps buffer valuation shocks. Lonvo-z’s progress could therefore become a near-term narrative stabilizer, particularly if forthcoming safety data at medical conferences reinforces a clean profile. In effect, while nex-z faces scrutiny, lonvo-z gives analysts a reason to keep the stock under watch rather than write it off completely. Its success could re-anchor Intellia’s long-term value proposition in the gene-editing landscape.

Financial Runway & Operational Flexibility

From a financial standpoint, Intellia appears to have sufficient liquidity to weather near-term turbulence. As of September 30, 2025, the small-cap biotech held $669.9 million in cash, cash equivalents, and marketable securities, compared to $861.7 million at the end of 2024. CFO Edward Dulac noted that the firm raised around $115 million through its ATM facility in the third quarter and expects its cash runway to extend into mid-2027—long enough to cover operations through lonvo-z’s expected commercial launch. While clinical holds halt patient dosing and may slightly reduce short-term spending, overall operating expenses remain substantial due to ongoing safety reviews, regulatory coordination, and research commitments. The company reported a Q3 2025 net loss of $101.3 million, improved from $135.7 million the prior year, aided by lower R&D expenses and restructuring initiatives. However, the temporary freeze on nex-z will likely shift cash utilization patterns and could delay anticipated milestone payments or future funding partnerships. In a small-cap biotech context, liquidity acts as both a defensive shield and a sentiment driver—investors gain confidence knowing the firm can sustain R&D without immediate dilution. Yet the longer the clinical hold persists, the greater the risk of valuation erosion if investors anticipate future capital raises or reduced pipeline visibility. The ability to maintain discipline while safeguarding the balance sheet will remain a critical factor in shaping market reaction.

Valuation Multiples & Market Repricing

Before the patient death, Intellia’s valuation had already fluctuated sharply through 2025, reflecting the inherent volatility of small-cap biotechs. As of November 10, 2025, the company traded at LTM EV/Revenue of 9.65x and LTM P/S of 19.59x, down from significantly higher multiples earlier in the year, such as 25.09x and 35.07x respectively in Q2. These contractions suggest that the market had begun adjusting for clinical risk even before the fatality announcement. The post-event decline—over 20% in a single session—implies that investors are now discounting both regulatory uncertainty and future cash flow compression. With LTM EV/EBITDA and EV/EBIT ratios both around -1.19x, the stock currently trades in deep negative territory, typical for development-stage small caps. Such valuations underscore limited short-term earnings visibility, but they also highlight that much of the company’s worth is tied to intangible pipeline optionality. In biotech terms, sentiment can swing from skepticism to optimism rapidly once regulatory clarity or positive data returns. For now, investors appear to be re-basing expectations to reflect a more cautious risk-reward profile, effectively resetting Intellia’s valuation closer to peers facing late-stage safety reviews rather than platform expansion.

Final Thoughts

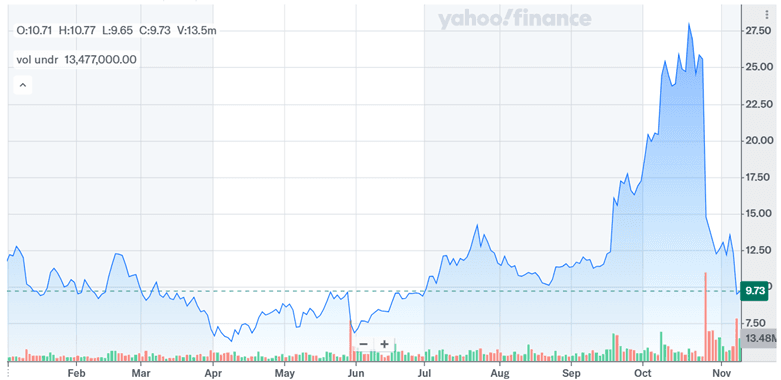

Source: Yahoo Finance

We can see Intellia Therapeutics’ stock crashing after the big news as shown in the above chart as the management continues to walk a tightrope. The death in its nex-z trial has shaken faith in its flagship program, and the FDA’s ongoing review means uncertainty will hang over the stock for some time. On the other hand, the company isn’t running out of options—or cash. With a financial runway stretching into mid-2027, an active dialogue with regulators, and real progress on its second major program, lonvo-z, there’s still meaningful work happening behind the scenes. Looking at valuation, Intellia’s LTM EV/Revenue multiple of 9.65x and Price-to-Sales ratio of 19.59x suggest that investors are still pricing in some long-term potential, even if confidence has wavered. For now, it’s all about balance—between optimism and realism, innovation and caution. Whether this small-cap biotech can bounce back will depend not on hype, but on how transparently and swiftly it rebuilds credibility with both regulators and investors.