Mobix Labs (NASDAQ:MOBX), a rising small-cap in wireless and interconnect solutions, has sparked market interest with its latest move to acquire Peraso Inc. (NASDAQ:PRSO). On September 5, 2025, the company sweetened its initial all-stock offer with a new cash component, valuing Peraso at approximately $1.20 per share—a 20% premium to its 30-day average through June 11. Peraso shares jumped nearly 25% in premarket trading on the news, highlighting investor optimism. Mobix Labs continues to scale its business via internal innovation, recent acquisitions such as Spacecraft Components Corp. and SCP Manufacturing, and deeper ties to U.S. defense and aerospace customers. The potential Peraso acquisition could unlock a range of technological and commercial synergies—provided Mobix can navigate integration risks and valuation hurdles effectively.

Expanding Millimeter Wave Capabilities In A Defense-First Strategy

Peraso's expertise in millimeter wave (mmWave) integrated circuits and antenna modules aligns closely with Mobix Labs' growing wireless portfolio, particularly the RaGE Systems product group and its ongoing collaborations with the U.S. Department of Defense. RaGE recently secured a Phase 1 SBIR grant for a next-generation satellite communications system-on-chip in partnership with UMass Lowell. By bringing Peraso’s mmWave IP and design know-how in-house, Mobix can potentially accelerate the development of low-power, high-frequency systems critical to space and defense infrastructure. Peraso’s silicon portfolio includes beamforming front-ends and phased array solutions that complement Mobix’s ambitions in radar imaging, secure communications, and satellite connectivity. Moreover, this alignment strengthens Mobix’s ability to deliver vertically integrated, high-reliability wireless systems to military customers. This fits squarely into Mobix’s broader growth strategy, which includes filtered USB connectors for Apache and Chinook helicopters and multi-sensor imaging systems for rail and infrastructure monitoring. Peraso also brings mmWave silicon that is commercially validated for unlicensed 60 GHz WiGig applications, opening adjacent growth markets in industrial IoT, factory automation, and secure point-to-point networking. Integration of Peraso’s mmWave IP could reduce Mobix’s reliance on external licensing agreements, lower bill-of-materials costs, and drive gross margin expansion toward its 60% long-term target. However, realizing this synergy will require efficient technical integration, especially given the specialized nature of mmWave packaging and testing, which has historically strained smaller semiconductor firms. Success here would deepen Mobix Labs’ defensibility in high-frequency wireless systems and support its credibility as a partner to defense and aerospace primes.

Enabling Vertical Integration In High-Reliability Interconnect Solutions

Mobix Labs has made strategic inroads into high-performance interconnects, particularly through EMI Interconnect Solutions, which now supplies filtered ARINC and USB connectors to next-generation aircraft electronics and U.S. Army helicopter platforms. Acquiring Peraso offers an opportunity to vertically integrate RF front-end silicon with Mobix’s connector systems, creating tightly coupled assemblies that deliver enhanced signal integrity and reduced electromagnetic interference (EMI) in harsh environments. Peraso’s mmWave ICs could be embedded directly into shielded connectors or interposer solutions designed by Mobix, streamlining assembly for OEMs in aerospace and defense. This kind of integration offers performance advantages in weight-sensitive and space-constrained applications, which is particularly valuable for avionics, missile systems, and space payloads. Additionally, Peraso’s IC packaging capabilities could be adapted to Mobix’s ruggedized connector formats, enabling better thermal and mechanical performance. From a cost structure standpoint, eliminating multiple suppliers across the signal chain allows Mobix to exert more control over quality, lead times, and unit economics. As the company scales its EMI connector line, vertical integration with silicon will likely improve pricing power and help Mobix better serve federal programs where Buy America and supply chain security are priorities. However, realizing these synergies will require CapEx investments in test and validation infrastructure and could stretch engineering bandwidth, particularly during ongoing integration of other pending acquisitions like SCP Manufacturing and Spacecraft Components Corp. Nonetheless, the opportunity to deliver a seamless, end-to-end signal transmission solution could solidify Mobix’s positioning with key Tier-1 aerospace and defense customers.

Broadening TAM Through Entry Into Wireless Consumer & Edge Applications

While Mobix Labs is largely focused on military and industrial markets, acquiring Peraso offers a bridge into commercial and consumer segments via Peraso’s WiGig and 5G mmWave products. Peraso has built application-specific transceivers for fixed wireless access (FWA), AR/VR headsets, and ultra-high-speed video streaming—segments that demand compact, low-latency wireless links. These offerings could help Mobix diversify its revenue base beyond defense, providing access to faster-growth verticals like smart cities, autonomous vehicles, and smart factories. This expansion also opens the door for Mobix to license or co-develop with OEMs in segments where its current direct customer relationships are limited. Moreover, by acquiring Peraso’s customer pipeline and reference designs, Mobix gains credibility in edge-computing markets where its own portfolio has been underpenetrated. Peraso’s IP portfolio also contains patents critical to the IEEE 802.11ad/ay standards, which could strengthen Mobix’s licensing and patent monetization strategy. If executed correctly, Mobix could position itself as a fabless OEM spanning commercial and defense-grade mmWave systems, a model that attracts both strategic customers and potential acquirers in the long term. However, diversification also brings new risks—namely, exposure to commoditized pricing dynamics and shorter product life cycles common in consumer electronics. Margins in these markets are typically lower, and success requires agile go-to-market execution, which Mobix has yet to demonstrate outside defense and aerospace. Balancing this diversification without diluting the company’s high-reliability brand will be key.

Leveraging Combined Scale For Operating Leverage & Financing Access

Mobix Labs has shown a disciplined approach to cost control, narrowing adjusted operating losses for four consecutive quarters and reporting a 54.1% gross margin in Q1 FY25. However, its limited scale—just $3.17 million in quarterly revenue—constrains its ability to spread fixed costs and attract favorable financing. Peraso, despite its own financial challenges, brings added scale, customer relationships, and potential revenue synergies. Consolidation could also support OpEx rationalization by eliminating duplicate R&D, sales, and G&A functions. This is particularly important as Mobix targets long-term adjusted operating margins of 30% while managing integration costs from other recent deals. From a capital markets perspective, a larger revenue base and diversified customer mix could enhance Mobix’s appeal to institutional investors and lenders, especially as it pursues new financing to support its acquisition strategy. On the investor relations front, a completed acquisition may boost perceived momentum and drive higher trading volumes, which could reduce capital-raising friction. However, Mobix’s trailing valuation multiples remain elevated relative to underlying fundamentals. As of September 5, 2025, Mobix trades at a trailing EV/Revenue multiple of 5.90x and an LTM P/S of 5.41x—high for a company still posting negative EBITDA and EBIT multiples of -1.73x and -1.63x, respectively. This premium valuation raises the bar for post-deal performance and leaves limited margin for error. Any missteps in integrating Peraso or failing to realize promised synergies could trigger multiple compression and reduce shareholder returns.

Final Thoughts

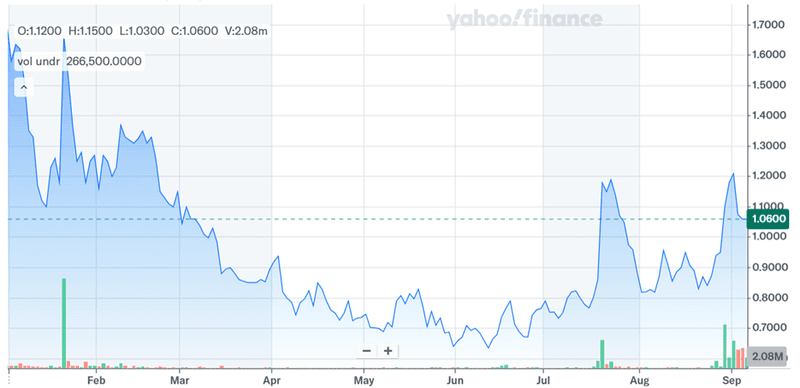

Source: Yahoo Finance

We can see a slight jump in Mobix Labs’ stock price after the unsolicited, sweetened cash-and-stock bid for Peraso which reflects a bold approach to accelerating scale and enhancing technological capabilities. We believe that the combined scale of the 2 entities may unlock operating leverage and improved capital access. Yet, execution risks are significant. Integrating Peraso alongside ongoing acquisitions like SCP Manufacturing could strain resources. Commercial diversification may dilute margins. Critically, Mobix’s premium valuation—5.90x EV/Revenue and 11.32x EV/Gross Profit—offers little room for underperformance. Overall, we believe that whether the transaction ultimately proceeds or not, it underscores Mobix’s ambition to become a more vertically integrated, technically differentiated player in the rapidly evolving wireless and aerospace tech landscape.