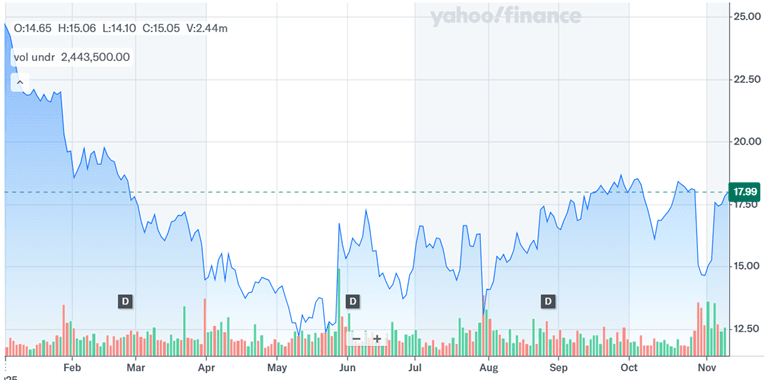

When a billionaire activist investor takes a major position in a small-cap auto repair chain, Wall Street pays attention. That’s exactly what happened when Carl Icahn revealed a nearly 17% stake in Monro Inc. (NASDAQ:MNRO), sending the stock soaring more than 15% last week. In response, Monro’s board quickly adopted a limited-duration shareholder rights plan, commonly called a poison pill, designed to prevent any investor from accumulating 17.5% or more of the company’s shares without board approval. The plan expires in one year, on November 6, 2026, and appears aimed squarely at slowing Icahn’s influence while the company continues its operational turnaround. Monro, which operates more than 1,100 auto repair and tire stores nationwide, has been under pressure for years due to weak margins, inconsistent same-store sales, and execution challenges. Now, as Icahn’s arrival fuels speculation about potential strategic shifts, investors are weighing whether this move signals opportunity—or brewing conflict.

Operational Turnaround & Cost Discipline May Support Upside

Despite its small-cap size, Monro has been aggressively rebuilding its foundation over the past year through a performance improvement plan focused on digital marketing, store optimization, and tighter cost control. Management under CEO Peter Fitzsimmons has closed 145 underperforming stores, improved inventory management, and introduced advanced merchandising analytics to refine tire pricing and demand forecasting. Gross margin expanded to 35.7% in the latest quarter—up 40 basis points year-over-year—while adjusted operating income climbed to $14 million, or 4.8% of sales, despite softer consumer trends. The company also generated $30 million in operating cash flow during the first half of fiscal 2026 and reduced net bank debt to $50 million, giving it financial breathing room. This operational discipline has been paired with customer segmentation work identifying high-value, repeat service customers—those who buy both tires and maintenance packages. Digital marketing efforts targeting these segments now span over half the store base and are showing measurable lifts in call volume, store traffic, and gross profit dollars. As Monro scales these initiatives across its footprint and completes its call center rollout, the potential for improved same-store sales and margin leverage could attract investors seeking steady, cash-generative retail names in a volatile market. Icahn’s presence may also act as a governance catalyst, increasing accountability and accelerating efficiency-focused decisions.

Activist Pressure Could Unlock Strategic Value

Carl Icahn’s nearly 17% stake introduces an entirely new dynamic for Monro. Icahn, long known for activist campaigns in automotive and industrial companies, has a history of pushing for operational streamlining, divestitures, or outright sales when he sees undervaluation. For context, Monro’s LTM EV/EBITDA multiple of roughly 10.2x and Price-to-Sales of 0.45x suggest it trades below historical sector averages for specialty retail and auto service peers. This discount could make it an appealing candidate for strategic buyers—perhaps private equity firms or larger aftermarket players seeking regional expansion. Icahn’s involvement could prompt board and management to review underperforming assets, consider real estate monetization beyond the current 40 owned stores being sold, or explore franchise and partnership models to lighten capital intensity. The activist angle could also push for accelerated dividend or buyback programs, given Monro’s 6.3% forward dividend yield and improving cash generation. Historically, Icahn’s interventions have often led to improved corporate governance and stronger capital allocation discipline, particularly in fragmented service industries where consolidation is ongoing. If Icahn plays a collaborative role rather than an adversarial one, his track record could help Monro realize underlying asset value and reposition itself from a sluggish regional player to a more strategic national service platform, potentially lifting shareholder returns over time.

Competitive & Consumer Pressures Threaten Recovery

The bullish case aside, Monro faces mounting structural and cyclical headwinds that no shareholder rights plan or activist influence can easily fix. The company continues to battle soft consumer demand, with October same-store sales declining about 2%, largely due to lower traffic. Its tire volumes were down mid-single digits during the latest quarter, reflecting price sensitivity among lower-income consumers—an important segment for Monro’s business model. While management argues that digital marketing and call-center initiatives will drive sustainable comps, these improvements may take time to offset the drag from a challenging macro environment. The small-cap chain also remains vulnerable to labor cost inflation, with technician wages up roughly 80 basis points year-over-year as a percentage of sales, eroding some of the benefits of cost reductions elsewhere. Moreover, tariffs on imported tires could further strain margins, especially if pricing power weakens amid competitive discounting from larger peers like Mavis, Discount Tire, and Goodyear’s retail network. Monro’s limited geographic diversification—heavily concentrated in the Eastern U.S.—also exposes it to regional economic swings. Even with vendor support and fall promotions, inventory turnover remains critical, and any missteps could tie up working capital just as interest rates remain high. These operational challenges suggest that while Icahn’s involvement adds intrigue, the road to sustainable growth is far from assured.

Poison Pill May Signal Management’s Defensive Stance

The board’s adoption of a poison pill—capping outside ownership at 17.5%—is a clear signal that Monro’s leadership wants time to execute its turnaround without interference. Yet it also raises governance questions. Poison pills are typically deployed to deter hostile takeovers, but they can also entrench existing management and frustrate shareholders seeking change. Icahn’s history with automotive businesses, including his prior ownership of Pep Boys, suggests he might push for strategic alternatives or management restructuring if results don’t improve. Monro’s plan is set to expire in one year, giving both sides a window to negotiate direction. However, if operational progress remains uneven, institutional investors may side with Icahn in demanding sharper accountability or board refreshment. The optics of adopting a poison pill immediately after an activist’s disclosure can spook investors who see it as defensive rather than constructive. While management cites the need to protect all shareholders from coercive tactics, the move could also delay potential value-unlocking scenarios. The balance between execution autonomy and shareholder influence will likely determine whether Monro’s next chapter is collaborative or contentious. In the meantime, this governance friction could inject volatility into a stock that already trades at modest valuation levels relative to peers.

Final Thoughts

Source: Yahoo Finance

Monro’s adoption of a poison pill following Carl Icahn’s 17% stake has resulted in wild movements in the stock price. The news has transformed what was once a quiet small-cap turnaround story into a potential activist battleground. Based on its latest LTM valuation multiples, including an EV/EBITDA of 10.18x, P/E of about 25x, and Price-to-Sales of just 0.45x, Monro appears moderately priced for a company in transition—neither deeply undervalued nor richly valued. Its high dividend yield of around 6% offers income support but also reflects investor skepticism about near-term growth. For now, Monro sits at a crossroads between incremental operational recovery and activist-driven strategic change. How these forces interact over the next year will determine whether this small-cap name remains in the slow lane—or finds a faster route to shareholder value.