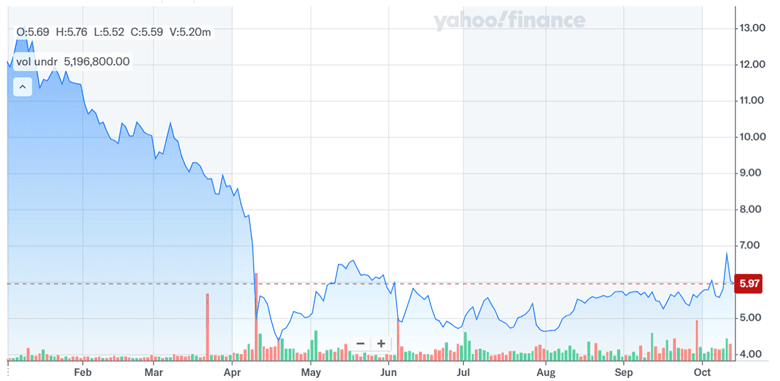

After a rough 2025, Neogen Corporation (NASDAQ:NEOG) finally caught a break. Shares jumped 23% on the heels of Q1 earnings that didn’t disappoint—and, just as importantly, a fresh cost-cutting plan that includes trimming 10% of its global workforce. That’s a bold move for a company still finding its post-3M integration footing. Even more surprising? Neogen didn’t backpedal on its full-year guidance. This small-cap has been through the wringer, down over 50% year-to-date before the announcement. But under new CEO Mikhael Nassif, the company is getting back to basics: cut costs, focus on core products, and stop trying to do too much at once. With earnings in line, revenues beating estimates, and investor sentiment no longer in free fall, Neogen might finally have a path to sustainable recovery. It’s early, yes—but this stock just reminded the market it’s not dead yet.

Earnings Beat Reinforces Market Confidence

For a company that’s been stumbling, just hitting expectations can feel like a victory—and that’s exactly what Neogen delivered. Q1 2026 adjusted EPS came in at $0.04, right in line with forecasts, while revenue of $209.2 million beat the Street’s $203.1 million call. The food safety side struggled a bit, falling 4.6% due to distributor hiccups and inventory normalization. But the animal safety segment showed strength, up 5.8% year-over-year, led by biologics and wound care. Adjusted EBITDA was $35.5 million, yielding a 17% margin—not amazing, but solid given tariff pressures and post-merger messiness. Free cash flow also saw a big improvement: only a $13 million outflow, way better than last year’s $56 million cash burn. This is what you want to see from a small-cap trying to turn the corner: modest but tangible progress. Inventory levels are being cleaned up, CapEx is more controlled, and operational focus is tightening. No fireworks here—but the lack of a negative surprise was enough to spark a relief rally.

Cost-Cutting & Layoffs Boost Margin Outlook

Neogen’s breakout moment wasn’t just about meeting numbers—it was about cutting fat without cutting muscle. The company announced it’s slashing $20 million in annual operating costs, starting with a 10% global headcount reduction. That includes jobs they hadn’t filled yet—so the real-world impact is more surgical than it sounds. About $12 million in savings will hit the current fiscal year, with half already baked into the outlook. The goal isn’t just to cut—it’s to get leaner and more nimble. CEO Nassif says the company’s structure had become bloated and slow. Now, they’re refocusing on core innovation and speeding up operations like sales planning and sample collection. The company’s also advancing the in-house shift of Petrifilm production, a move that could remove $15 million in duplication. Of course, cost cuts always come with risks—especially when execution has been a weakness. But so far, the messaging is clear: Neogen isn’t retreating, it’s realigning. And if the business can hold the line on revenue, these savings could finally start showing up in margins.

Reaffirmed Guidance Signals Management Confidence

The market loves clarity—and for small-caps under pressure, reaffirming guidance is often the biggest vote of confidence a CEO can give. Neogen didn’t just avoid a downgrade—it held steady on its full-year fiscal 2026 outlook despite distributor noise, integration hangovers, and a still-shaky sample collection line. This suggests the company has a decent handle on what’s coming next. Management expects Q2 to be stronger than Q1, which is typically seasonally soft. The genomics unit, currently up for sale, remains part of the guide for now but will be pulled once the deal closes. Also worth noting: even with headline softness in Petrifilm, underlying U.S. distributor sales remain solid. Animal Safety, too, is showing signs of health, especially in high-margin areas like life sciences reagents. Leadership says it has the talent and contingency plans to manage the Petrifilm handoff internally—a relief to investors burned by earlier delays. After a year of missed targets and credibility hits, sticking to guidance is a small but meaningful win. Investors don’t need perfection—they just need predictability.

Execution & Growth Sustainability Risks

Of course, this isn’t a victory lap yet. Neogen still faces real risks—especially around execution. The company’s recent history includes inventory write-offs, sample collection inefficiencies, and supply chain headaches that eroded margins and trust. The sample collection line is particularly stubborn, with high scrap rates and poor utilization dragging on profitability. Fixes are underway, but meaningful improvement may not show up until late 2026. Meanwhile, the innovation pipeline is running lean. Years of focus on integrating 3M’s food safety assets have sapped R&D resources. The new strategy is to do fewer things better—but no timeline has been given for major new product launches. Market share losses in niche categories like allergens and natural toxins don’t help either. Neogen is still carrying $800 million in gross debt, and while Q1 saw a $100 million paydown, free cash flow remains fragile. CapEx is still elevated, and working capital needs haven’t disappeared. For a small-cap, the path to recovery looks viable—but it’ll take near-perfect execution to get there. Investors should keep expectations grounded.

Final Thoughts

Source: Yahoo Finance

Neogen’s stock surge is a welcome change of pace—and possibly the first real sign of traction under new leadership. From a valuation standpoint, Neogen trades at 19.53x LTM EV/EBITDA and 2.22x LTM EV/Revenue—not cheap for a company with negative earnings and execution challenges, but not unreasonable if the margin trajectory keeps improving. The Q1 beat, sharp cost discipline, and reaffirmed guidance paint the picture of a small-cap getting its act together. That said, the turnaround is still early, and the risks are real. Inventory fixes, manufacturing transitions, and a tighter product focus all need to click to unlock sustainable growth. Small-cap turnarounds can be bumpy, but they also offer asymmetric upside. Investors should stay cautious—but not dismissive. Neogen may have more left in the tank than its recent stock chart suggests.