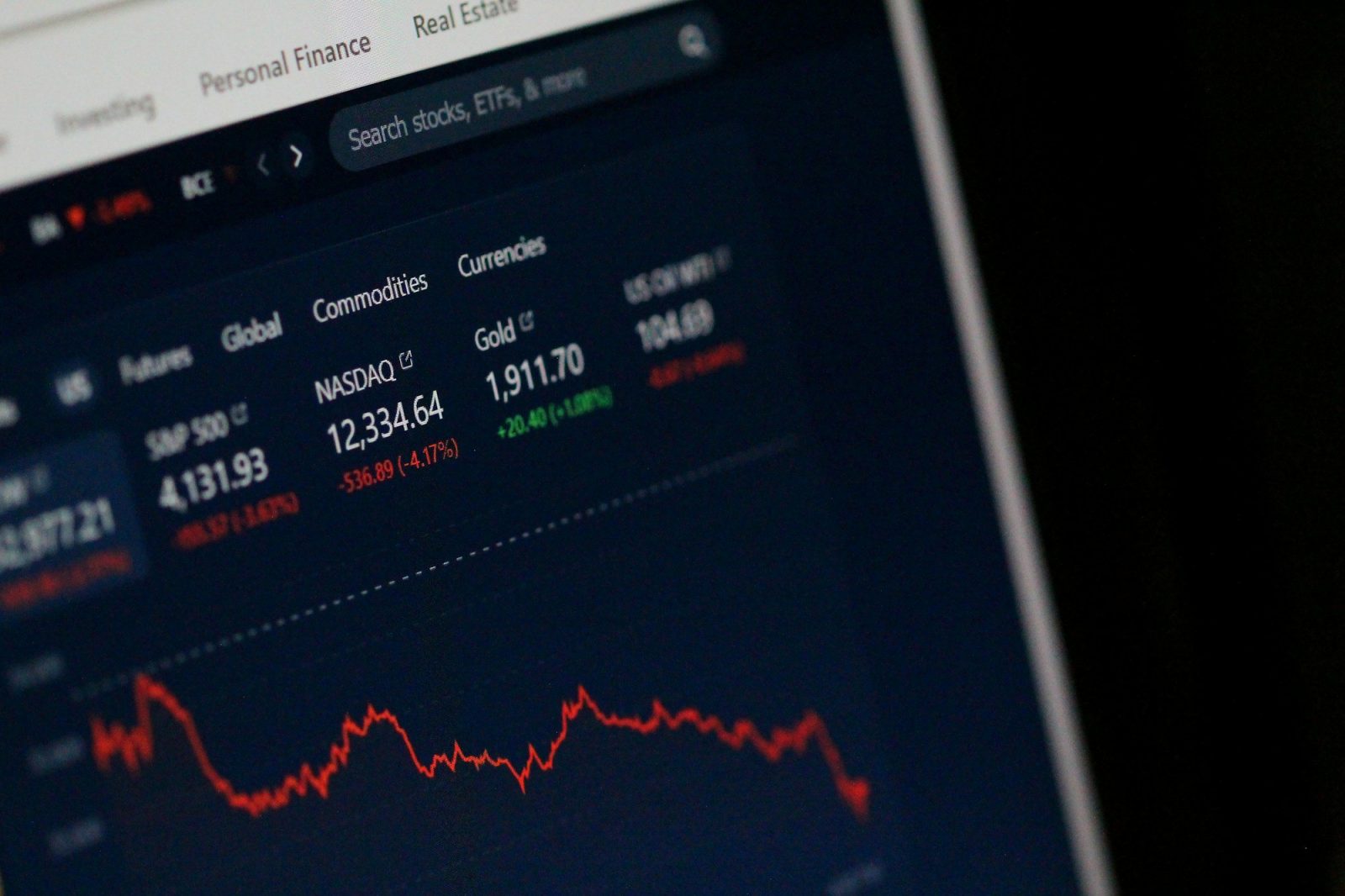

U.S. stocks edged lower on Wednesday as AI-driven growth prospects and rising geopolitical uncertainty in the Middle East took focus. The major indexes pulled back from recent record highs as escalating tensions involving Iran, Israel, and regional military activity pushed energy prices higher and reignited concerns about inflation.

The Dow Jones Industrial Average fell roughly 0.8%, while the S&P 500 declined about 0.5%. The Nasdaq Composite also retreated as gains in select semiconductor and AI-related names were offset by weakness across software, cybersecurity, and growth stocks. Rising oil prices and renewed questions about the trajectory of Federal Reserve policy added another layer of caution to an otherwise resilient market backdrop.

Market Movers:

- Navitas Semiconductor (NVTS) +25%: Shares surged after the company highlighted its collaboration with Nvidia on next-generation power solutions for AI data centers. Investors viewed the partnership as a significant opportunity for Navitas to capitalize on rapidly growing demand for high-performance AI infrastructure.

- GameStop (GME) +9%: The retailer rallied after reporting strong first-quarter profitability and announcing a new $2 billion share repurchase program. Investors also reacted positively to management's continued efforts to deploy its sizable cash position toward strategic growth initiatives.

- Marvell Technology (MRVL) +5%: Shares extended recent gains as enthusiasm surrounding AI networking and custom silicon demand remained strong. Investor sentiment continued to benefit from growing expectations that Marvell will play a central role in next-generation AI data center deployments.

- Medtronic (MDT) +5%: The medical technology giant advanced after reporting better-than-expected quarterly results driven by strong cardiovascular product demand. Growth in cardiac ablation technologies and market share gains helped offset concerns about slightly softer earnings guidance.

- Intel (INTC) +5%: Shares moved higher after executives emphasized accelerating demand for data center processors and growing production of advanced manufacturing nodes. Investors welcomed management's optimism surrounding AI-driven computing demand and operational restructuring efforts.

- Intuitive Machines (LUNR) -8%: The space infrastructure company fell after announcing plans for a new at-the-market stock offering. The prospect of additional share issuance weighed on sentiment despite continued enthusiasm surrounding the broader space sector.

- GitLab (GTLB) -5%: Shares declined after the company unveiled a restructuring plan that includes workforce reductions and a narrower geographic footprint. Investors focused on the near-term costs associated with the changes despite management's long-term growth rationale.

- Palo Alto Networks (PANW) -5%: The cybersecurity leader slipped despite posting strong quarterly results and raising guidance. Investors appeared to lock in profits following a powerful rally in cybersecurity stocks and looked for even stronger upside relative to elevated expectations.

Oil Prices Rise as Middle East Risks Escalate

Energy markets remained in the spotlight. Crude oil prices traded higher after reports of renewed military activity involving Iran and additional regional instability raised concerns about the security of global energy supplies. West Texas Intermediate crude traded above $95 per barrel while Brent crude approached $97. The ongoing uncertainty surrounding negotiations to reopen critical shipping routes through the Strait of Hormuz continues to support elevated energy prices and poses a potential inflation risk for the global economy. Higher oil prices have increasingly become a concern for investors, policymakers, and consumers alike, particularly as summer travel demand begins to accelerate.

Strong Labor Market Data Supports Economic Resilience

Fresh labor market data offered a more encouraging picture of the U.S. economy. ADP reported that private employers added 122,000 jobs in May, while earlier JOLTS data this week showed job openings remaining stronger than expected. The figures suggest the labor market remains resilient despite elevated interest rates and ongoing geopolitical uncertainty. Investors are now focused on Friday's nonfarm payrolls report, which could provide important clues about the Federal Reserve's next policy moves. At the same time, some Fed officials have warned that persistent inflation pressures may require a more restrictive policy stance if recent price trends continue.

AI Investment Boom Continues Despite Market Pullback

While broader markets struggled, the AI investment theme remained one of the strongest drivers of corporate activity. Meta announced new monetization efforts for its business-focused AI agent offerings, expanding revenue opportunities across WhatsApp, Messenger, and Instagram.

Meanwhile, Nvidia's ecosystem continued to lift suppliers and infrastructure partners throughout the semiconductor sector. Companies tied to AI networking, power management, servers, and data center expansion have remained among the market's strongest performers even as investors rotate away from portions of the software sector. The divergence highlights a key trend in 2026: investors remain highly selective within the AI trade, favoring infrastructure providers over some application-layer software companies.

Looking Ahead

Markets now face an important stretch as investors monitor both geopolitical developments and incoming economic data. Friday's jobs report will provide the next major test for expectations surrounding interest rates, while any progress or setbacks in U.S.-Iran negotiations could significantly impact energy markets. At the same time, earnings season is nearing its conclusion with key reports from AI and cybersecurity companies still in focus. If labor market data remains strong and oil prices stabilize, investors may regain confidence in the broader rally. However, persistent geopolitical risks and higher energy costs could create additional volatility as markets attempt to build on their recent record-setting run.