Viomi Technology (NASDAQ:VIOT) just got investors talking again. The Chinese smart home and water purification company saw its stock jump after announcing a $20 million share buyback plan that runs through the end of 2027. That is a big move for a small-cap stock like Viomi, and it came right after the company wrapped up a huge business overhaul to focus purely on its home water systems. The company says that it is using cash already on hand to fund the buyback — no debt involved. For investors, that sounds like a management team confident in its turnaround story. Between the return to profitability, new international growth plans, and a sharper business focus, Viomi seems to be winning back some trust on Wall Street. But as with any small company coming out of restructuring, there are still risks. Let’s dig into what’s driving the excitement — and where caution might still be needed.

Viomi’s Big Pivot To Smart Water Solutions Is Paying Off

So what’s changed at Viomi? The short answer: everything. In 2024, the company decided to sell off its older smart home appliance business and double down on what it does best — water purification systems powered by AI. That means focusing on things like water filters, purifiers, and heaters with built-in tech that makes them easier to use and maintain. The results have been pretty eye-catching. For the full year 2024, Viomi’s revenue hit RMB 2.1 billion (that’s up 29% year over year), and it swung from losses to a profit of RMB 62 million. The company’s Kunlun and Vortex product lines have been standouts — offering everything from instant cooling and mineralized water to DIY filter changes. The Vortex line even debuted on Kickstarter, blowing past its funding goal in a single day before hitting Amazon US. On the home front, Viomi’s Kunlun AI Water Purifier ranked in the top 10 on Douyin, Pinduoduo, and Tmall during China’s massive Double 11 shopping event. The company also showed off its new line at CES 2025 in Las Vegas and built new retail partnerships in Malaysia to reach more customers. Its Water Purifier Gigafactory — yes, that’s the name — handles nearly all production in-house, keeping costs under control and quality consistent. Viomi has also streamlined its marketing with an Integrated Product Marketing System (IPMS) that ties its products, branding, and sales under one roof. All this trimming and refocusing helped Viomi lower its overall expense ratio by 6% last year and end 2024 with over RMB 1 billion in cash. For a small-cap company that was struggling not long ago, this is a pretty solid turnaround story.

The Buyback Shows Management Is Confident & Careful With Cash

Now, let’s talk about that $20 million buyback — the news that lit up the stock. For a company the size of Viomi, that’s not a token gesture. It’s a signal. When a board authorizes a repurchase plan like this, it’s basically saying, “We think our stock is cheap, and we believe in where we’re headed.” Viomi plans to fund the buyback entirely from existing cash — and it has plenty. As of the end of 2024, Viomi was sitting on over RMB 1 billion in cash and equivalents, so this move doesn’t stretch its balance sheet. The timing makes sense too. After a solid financial recovery in 2024, with non-GAAP profits reaching RMB 79.9 million, management clearly wants to show investors that this turnaround isn’t just a one-off. Looking at the numbers, Viomi still trades at some very modest valuation levels: just 0.79x price-to-sales and 2.84x EV/EBITDA on a trailing basis. Those figures are way below what similar tech-driven appliance makers fetch in the market. The buyback could also help counter any dilution from stock-based compensation while giving management more control over capital returns. For investors, especially those watching small-cap names, buybacks like this can be a big vote of confidence — and a hint that the leadership team feels the market isn’t giving them enough credit for the progress they’ve made so far.

Expanding To The U.S. & Southeast Asia Could Be A Game Changer

Viomi isn’t just cleaning up at home — it’s going global. Its “Global Water” strategy is all about taking its tech and design know-how to new markets, and the early signs look promising. In the U.S., Viomi launched its Vortex under-sink water purifiers on Amazon, and the feedback has been great. About 80% of users said installation took under 20 minutes, and many liked that it’s a tankless system that saves both time and space. Over in Southeast Asia, Viomi has teamed up with Malaysia’s biggest home appliance retailer to get its products into more homes — a move that could help it grab market share fast. The company’s CES 2025 showcase in Las Vegas was also a turning point, giving Viomi some global exposure as a “smart water” brand rather than just another appliance maker. With nearly 1,800 patent filings worldwide and a fully in-house production model, Viomi’s ready to compete on both innovation and cost. Its Gigafactory setup lets it scale production quickly and ensure that new products — like ice-making purifiers and instant-cooling systems — reach global markets faster. This expansion isn’t just about sales; it’s about survival. The Chinese market for appliances has gotten crowded and price-sensitive, so building a brand that resonates overseas helps balance things out. If Viomi can continue tailoring products for local needs while keeping quality high, its international growth could be the biggest catalyst for long-term stability.

Margins Are Still Squeezed & Competition Is Heating Up

Of course, it’s not all smooth sailing. Viomi’s margins took a noticeable hit last year. Its gross margin dropped to 25.9% in 2024, down from 31.9% the year before, and that slide continued in the back half of the year. Why? Product mix. The company sold more low-margin products like water heaters and bundled kitchen appliances, especially through its Xiaomi partnership, and fewer high-margin consumables like replacement filters. Those filters are usually the profit drivers, but sales to Xiaomi fell 14.5% last year, which stung a bit. On top of that, marketing costs went up, with Viomi spending more on online promotions to build brand recognition. The result is a business that’s growing fast but not yet expanding margins. Competition is also intensifying both in China and abroad, where other players are racing to capture the same water purification opportunity. To keep its edge, Viomi needs to boost sales of its consumables — the kind of recurring revenue that can smooth out profitability — and maintain premium pricing for its newer AI-driven models. Right now, its valuation multiples have improved — LTM EV/EBITDA is up to 2.84x and EV/EBIT to 4.01x — but they’re still far below industry averages. The company has definitely made progress, but margin stability will be the real test of whether this turnaround can last.

Final Thoughts – Is Viomi’s Jump Justified?

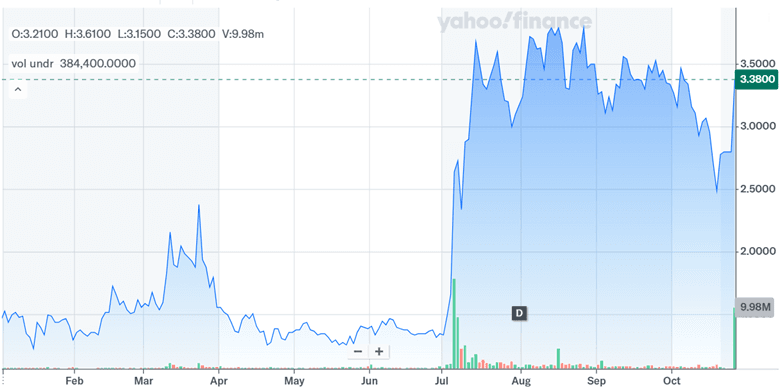

Source: Yahoo Finance

We can see the big jump in Viomi’s stock price in the above chart along with the surge in volumes. Its $20 million buyback definitely make sense in light of everything that’s been happening. The company has pulled off a full-scale reset: it’s profitable again, running leaner, and focusing on a core business that’s actually growing. It’s also expanding internationally at a smart pace and signaling confidence with its capital return strategy. On the flip side, Viomi still has to prove it can keep its margins healthy while growing its premium and consumables sales. Valuation-wise, it’s still trading at small-cap levels — around 0.79x price-to-sales, 2.84x EV/EBITDA, and 11.61x P/E on a trailing basis. That makes it one of the cheaper tech-enabled appliance stocks out there. Whether that discount remains or starts to close depends on what happens next with margins and product mix. For now, Viomi’s buyback has put it back on investors’ radar — and it’s one small-cap worth watching as it continues its global “smart water” journey.