Olema Pharmaceuticals (NASDAQ:OLMA) is rapidly evolving from a small-cap biotech story into a serious strategic chess piece in the hormone receptor-positive (HR+) breast cancer space. The company’s recently announced clinical trial and supply agreement with Pfizer to evaluate its lead drug, palazestrant, in combination with Ibrance (palbociclib) comes just months after securing a similar partnership with Novartis for use alongside Kisqali (ribociclib). These two CDK4/6 inhibitors dominate the frontline landscape in HR+/HER2- metastatic breast cancer and now place Olema in the strategic crosshairs of two of the “big three” in breast cancer—leaving Roche as the third wheel, for now. However, this may not last long. Roche is on the cusp of releasing results from its PersevERA trial evaluating giredestrant, a competing oral SERD. If the trial fails to deliver positive results, it could significantly enhance the scarcity value of Olema’s palazestrant. In that scenario, with Novartis and Pfizer already engaged, and Olema showing clinical progress and financial readiness, Roche may be forced to act, potentially sparking a bidding war. Let’s examine the key dynamics that could fuel such a scenario.

Strategic Pharma Partnerships as Validation

Olema’s twin collaborations with Pfizer and Novartis represent a pivotal inflection point, transforming the company from a high-risk clinical-stage asset into a strategically validated oncology player. In July 2025, Pfizer agreed to supply Ibrance for a combination trial with Olema’s palazestrant in ER+/HER2- metastatic breast cancer, following Novartis’ earlier decision to evaluate palazestrant with Kisqali in the OPERA-02 Phase 3 trial. The timing and sequencing of these alliances are significant. With both companies holding dominant market share in CDK4/6 therapies, their willingness to co-develop with Olema underscores confidence in the mechanism and combinability of palazestrant. From a strategic lens, these agreements effectively put two of the three major players in the HR+ metastatic space “at the data table” alongside Olema. That in itself raises competitive tension. Should palazestrant emerge as a best-in-class complete estrogen receptor antagonist and degrader (CERAN/SERD) with demonstrated synergy across both Ibrance and Kisqali, the strategic optionality narrows quickly. While these agreements are non-exclusive and do not constitute commercial deals, the data co-ownership and clinical engagement dynamics are critical. Both Pfizer and Novartis now have early access to combination data that could inform internal portfolio decisions, M&A discussions, or competitive blocking maneuvers. At a time when SERD assets have seen mixed clinical results across the industry, Olema’s ability to attract back-to-back big pharma partners is a strong indicator that palazestrant may be more than just another SERD—it could be a foundational backbone therapy in HR+ breast cancer. That makes it strategically valuable to own, not just partner.

Palazestrant’s Differentiation & Clean Global Rights

Palazestrant (OP-1250), Olema’s lead candidate, continues to show a favorable profile across multiple dimensions: mechanism, combinability, tolerability, and regulatory traction. It is a dual CERAN/SERD that completely blocks estrogen receptor (ER) signaling in both wild-type and mutant breast cancer, offering broad utility across patient segments. The drug has shown activity as a monotherapy and in combination with CDK4/6 inhibitors in early studies, and is currently being tested in the pivotal OPERA-01 Phase 3 trial for 2L/3L patients and the OPERA-02 frontline trial with ribociclib. Importantly, Olema recently finalized the 90mg dose for these trials, signaling alignment with regulators and enabling faster enrollment and development clarity. Unlike earlier-generation SERDs such as giredestrant and amcenestrant, which failed to meet efficacy endpoints in major trials, palazestrant has yet to show significant clinical red flags. Moreover, it has been granted Fast Track designation by the FDA, another signal of regulatory confidence. Olema is also exploring combinations with palbociclib, alpelisib, and everolimus, giving the drug broad applicability across treatment lines and resistance mechanisms. Financially, the company ended Q2 2025 with $362 million in cash, sufficient to fund operations through multiple catalysts, including top-line data from OPERA-01 in H2 2026. This liquidity gives Olema the ability to stay independent and push through late-stage development—unless a compelling offer emerges. All of this supports the idea that palazestrant is not just another pipeline asset but a potential endocrine backbone therapy, which could drive commercial leadership in HR+ breast cancer and reshape big pharma portfolios.

Roche’s Persevera Trial As A Key Catalyst

The most near-term external catalyst that could force the M&A narrative into motion is Roche’s impending PersevERA trial readout. The trial evaluates giredestrant, Roche’s own oral SERD, in a similar HR+/HER2- metastatic population. Results are expected any day. The outcome could be binary for the strategic positioning of Olema. If Roche's SERD disappoints—similar to the failures of Sanofi’s amcenestrant and other oral SERDs—it may mark the final derailment of internal SERD programs across big pharma. That would elevate Olema as a rare remaining independent player with a late-stage, promising ER-targeted agent. With Novartis and Pfizer already aligned, Roche would face a narrow window to secure strategic exposure to the space without being boxed out by competitors. Moreover, the combinability of palazestrant with multiple CDK4/6 inhibitors is particularly threatening to Roche’s downstream portfolio interests. Even if PersevERA posts positive data, Roche may still view Olema as an attractive hedge or complementary mechanism, particularly given the dual CERAN/SERD approach of palazestrant, which offers potential efficacy in resistant tumors. But a failure would shift the calculus entirely: Roche may have no choice but to acquire Olema to maintain competitive parity. In such a scenario, with two other majors already at the table, a bidding war becomes not just possible—but likely.

M&A Speculation & Market Reaction

The total enterprise value remains within striking distance for large-cap pharma, especially if the acquisition is seen as defensive (to block a rival) or synergistic (to deepen an existing CDK4/6 portfolio). Rumors of strategic interest from multiple parties, while not confirmed, have started to circulate following the Pfizer news. The narrative here is not just about data—it’s about timing, portfolio defense, and strategic exclusivity. If palazestrant becomes a linchpin asset, the competitive stakes will escalate quickly. With the PersevERA readout looming, the M&A window could narrow fast, adding urgency to any potential buyout bid.

Final Thoughts

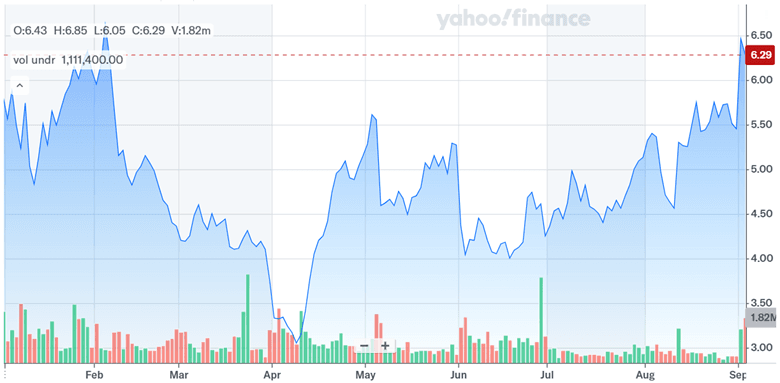

Source: Yahoo Finance

As we can see in the above chart, Olema’s stock surged 19% following the Pfizer partnership announcement, reflecting investor belief that the collaboration enhances the company’s strategic profile. However, the valuation still remains depressed on fundamental metrics. As of September 3, 2025, Olema trades at deeply negative valuation multiples. Its LTM EV/EBITDA and EV/EBIT both stand at -0.49x, while its LTM P/E is -3.25x. Even forward-looking metrics are underwater, with NTM EV/EBITDA and EV/EBIT at -0.43x and -0.40x, respectively. This indicates investor skepticism around the timing and scalability of revenue, which is typical for pre-commercial biotech firms. However, for an acquirer with a long-term horizon and oncology infrastructure—such as Pfizer, Novartis, or Roche—these multiples reflect optionality rather than risk. Overall, we believe that given the $362 million in cash, minimal liabilities, and a clean balance sheet, Olema could be acquired with minimal integration complexity.