Premier Inc. (NASDAQ:PINC) is the hottest small-cap in the spotlight today as a potential buyout candidate. It is rumored that Patient Square Capital, a healthcare-focused private equity firm led by former KKR executive Jim Momtazee, is exploring an acquisition of the Charlotte-based healthcare services and technology company. The deliberations are still in the early stages, and while there’s no guarantee of a deal, the firm is reportedly arranging financing for a potential take-private transaction. However, Patient Square has a track record of healthcare investments, having recently acquired Syneos Health and Patterson Cos., and may see Premier as a strategic fit. Let us dive deeper into these rumors and analyze the rationale behind Patient Square Capital’s potential interest and the possible synergies from a deal.

Deep Market Penetration In Healthcare Supply Chain Services

Premier’s Supply Chain Services segment continues to outperform expectations, underscoring the stability and scale of its GPO model. The company facilitates cost efficiencies for healthcare providers through aggregated purchasing power, enabling hospitals and systems to procure essential medical supplies, pharmacy products, and food services at reduced rates. As of FY2025, gross administrative fees from this segment grew 3%, with the expectation of accelerating to 4% growth in FY2026. Premier’s high-margin categories—such as MedSurg, pharmacy, and food—are gaining traction among both existing and non-member organizations. Notably, the pharmacy and food verticals are functioning as entry points for future broader GPO engagement. Additionally, Premier has completed major contract renewals under its 2020 restructure, with only 20% of that cohort's fees left to renegotiate, bringing greater clarity to future fee share stabilization, which is expected to level in the high-60% range. Patient Square may view this business as a stable cash generator with long-term visibility, offering defensive characteristics during economic uncertainty. The appeal is further heightened by Premier’s digital supply chain and co-management operations, both of which are growing double digits. These scalable, recurring-revenue models provide a foundation for value creation through operational optimization, bolt-on acquisitions, and accelerated digital adoption—tactics well within the wheelhouse of a healthcare-specialist PE firm like Patient Square.

Advisory Services Momentum & Enterprise-Wide Strategic Engagement

Premier has been aggressively revitalizing its Performance Services segment, especially the Advisory Services unit, which has become a standout growth engine. In FY2025, the company closed four large multi-year advisory contracts and expects the segment to grow over 25% in FY2026. These engagements target systemic transformation across revenue optimization, workforce productivity, clinical delivery, and supply chain improvements. With industry headwinds mounting—Medicaid reimbursement cuts, rising labor costs, and tightening margins—hospital systems are increasingly shifting from short-term cost containment to structural changes. Premier’s trusted reputation and integrated offerings position it as a preferred partner for such transformation. Patient Square likely sees significant synergy here, as the firm can help scale Premier’s advisory capabilities and extend them across its healthcare portfolio. The advisory business, sized between $50 million and $100 million annually, provides not only recurring consulting revenue but also acts as a wedge for cross-selling software and analytics tools. Premier’s unique integration of advisory talent and tech infrastructure enhances stickiness and unlocks multiple monetization channels. Furthermore, these engagements are milestone-based, ensuring performance-linked revenue streams with back-end loaded revenue recognition, creating stable, predictable cash inflows once the projects scale—an attractive feature for any private equity operator seeking internal rate of return (IRR) consistency.

Strategic Tech Assets & Real-Time Clinical Decision Capabilities

Premier’s technology ecosystem has received a meaningful boost with the recent acquisition of IllumiCare, a real-time clinical decision support platform that leverages AI to deliver savings of roughly $100 per inpatient discharge. The solution complements Premier’s existing Stanson Health platform and extends its addressable market by enhancing both clinical and financial performance for provider clients. In FY2026, IllumiCare is expected to contribute $8–10 million in revenue while breaking even on the bottom line, indicating a high-growth but low-risk expansion. The integration of real-time clinical and financial decision support tools positions Premier uniquely at the intersection of operations and patient care—an area Patient Square could exploit through capital investment and expanded go-to-market initiatives. Moreover, these tools have a proven 10:1 ROI for customers and work across all major EMR systems, giving them high scalability. The firm’s increased focus on SaaS solutions, particularly in prior authorization and clinical documentation powered by machine learning and NLP, fits well with Patient Square’s strategic preference for healthcare automation and efficiency tech. With enterprise software renewals expected to rebound in FY2027 and strong customer interest despite regulatory uncertainty, Patient Square could view this tech backbone as a critical asset with high embedded optionality. Owning this in a private setting could enable accelerated R&D, faster integrations, and larger bundled offerings across a broader healthcare ecosystem.

Attractive Valuation Amidst Stabilizing Financial Performance

From a financial standpoint, Premier Inc. appears attractively valued relative to its historical averages and industry peers. As of September 5, 2025, The company reported FY2025 free cash flow of $181 million with a conversion ratio of 69%, and expects FY2026 free cash flow conversion to reach 70–80%. With the termination of its tax receivable agreement (TRA) complete as of July 1, 2025, Premier’s cash flow profile will improve by ~$100 million annually, creating more internal capital for growth or leverage optimization. Patient Square could exploit this by implementing a leveraged buyout (LBO) strategy, using predictable cash flows to support debt service while targeting margin expansion in Performance Services and operational efficiencies in Supply Chain Services. However, rising NTM EV/EBIT and P/E multiples—currently at 21.51x and 18.87x respectively—suggest growing market expectations. Patient Square would need to justify the premium through aggressive synergy realization and top-line acceleration in the advisory and tech businesses, which are still in scaling mode.

Final Thoughts

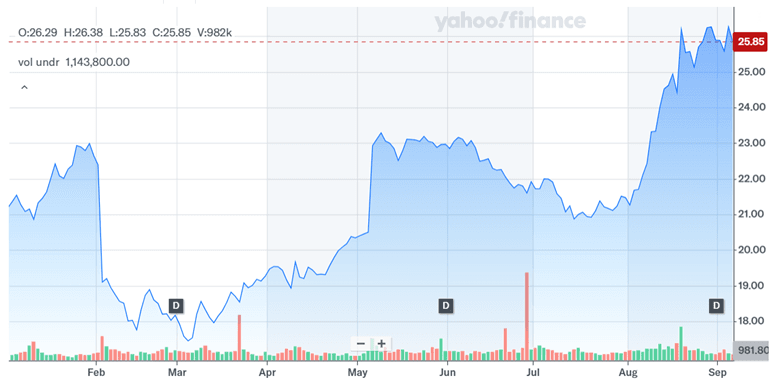

Source: Yahoo Finance

As we can see in the above chart, Premier’s stock has climbed 22% year-to-date, reflecting increased investor optimism amidst the strategic interest. The company trades at a trailing EV/EBITDA multiple of 8.18x and an EV/Revenue multiple of 2.30x. On a forward basis, the NTM EV/EBITDA is 10.12x and the NTM EV/Revenue is 2.38x. These multiples have expanded in recent quarters, reflecting both operational outperformance and speculation around a potential transaction. Nonetheless, they remain within reasonable bounds for a healthcare technology and services hybrid, particularly given Premier’s free cash flow profile. While Premier’s low free cash flow tax burden and completion of the TRA boost its attractiveness as an LBO candidate, we believe that the ultimate feasibility of a transaction may hinge on Patient Square’s conviction in realizing synergies and navigating healthcare’s shifting regulatory terrain.