There is a lot of drama brewing at Priority Technology Holdings (NASDAQ:PRTH) right now, and if you are a shareholder or just keeping an eye on small-cap fintech names, you will want to pay attention. One of the company’s biggest investors just came out swinging, saying the CEO’s offer to buy out the rest of the company and take it private is way too low. This investor, Steamboat Capital, owns a pretty large chunk of shares and thinks Priority is worth much more—especially after the company just reported some solid numbers for the quarter. In fact, they’re pushing the board to create a special committee of independent directors to look at all possible options, not just this offer. Why now? Because Priority’s business is improving, particularly in areas that bring in steady revenue and strong margins. So the big question is whether this offer is just bad timing or an intentional lowball move. With the CEO already owning more than half the stock, it is shaping up to be a real power struggle over who gets to decide what happens next—and at what price.

Undervaluation Claim & Upside Probability

Steamboat Capital’s assertion that the CEO’s $6.15-per-share ceiling “grossly undervalues” Priority Technology stems from a widening gap between the company’s improving financial profile and the implied valuation embedded in the take‑private proposal. Priority has evolved from a traditional merchant acquirer into a diversified small-cap fintech platform whose earnings increasingly rely on higher‑margin Payables and Treasury Solutions, which together now generate more than 60% of adjusted gross profit and contribute significant recurring revenue. In Q3 alone, these segments delivered 14% and 18% revenue growth, respectively, and helped push gross margin expansion to nearly 140 basis points year‑over‑year while also supporting rising adjusted EBITDA. The company added nearly $200 million in incremental deposits under administration—the largest quarterly increase in its history—reflecting stronger embedded treasury demand and validating the scalability of Priority’s “Connected Commerce” vision. Despite modest revenue growth in Merchant Solutions due to macro softness in restaurants, construction, and wholesale trade, Priority maintained stable merchant attrition and even saw sequential improvement into October. From a valuation standpoint, Priority’s current LTM multiples—such as an LTM EV/Revenue of 1.50x and EV/EBITDA of 7.26x—suggest a discount to peers in payments, embedded finance, and treasury automation, especially given its double-digit EBITDA CAGR since going public in 2018. Steamboat Capital believes that, under an arms‑length private transaction or alternative bidder, Priority could command a materially higher valuation multiple due to its recurring revenue mix, scalable API‑driven platform, and strengthening free cash flow profile, which totaled $71 million year‑to‑date and equates to roughly $1.17 per share on an annualized basis. This upside case is strengthened by the company’s strategic progress—including two recent acquisitions (Boom Commerce and Dealer Merchant Services), real‑time payment capabilities, Canadian acquiring activation, and a nonrecourse residual financing facility designed to accelerate ISV and ISO growth. Investors arguing undervaluation point to these structural tailwinds as evidence that the CEO’s offer may be opportunistic, captured at a time when Priority’s intrinsic value is not fully reflected in the public markets.

Special Committee & Strategic Alternatives As Value Catalysts

Steamboat Capital’s call for the formation of a special committee of independent directors represents a pivotal moment for Priority Technology, as it introduces potential value‑unlocking pathways that were not previously on the table. With the CEO holding a controlling stake, minority shareholders rely heavily on board independence to ensure that any proposed transaction—whether a take‑private or a sale—reflects true fair value. The request for a special committee indicates that investors want an unbiased evaluation of strategic alternatives, including soliciting competing bids, performing a full valuation analysis, hiring external advisors, and exploring options such as minority recapitalizations, asset carve-outs, or an outright sale to strategic or financial players. Priority’s recent financial performance strengthens the case for such a process: the company delivered adjusted EBITDA of $57.8 million in Q3, posted 12% year‑to‑date gross profit growth, and modestly raised full‑year EBITDA guidance to $223 million to $228 million despite macro headwinds. Moreover, the strategic mix shift toward recurring revenue—now over 64% of adjusted gross profit—enhances predictability and could appeal to buyers seeking stable cash‑flowing fintech assets. A structured process could also help surface interest from payments acquirers, treasury automation providers, embedded finance platforms, or private equity firms that may view Priority’s diversified platform, strong partner pipeline, and scalable API infrastructure as acquisition catalysts. A competitive environment could materially raise the clearing price well beyond the CEO’s bid, especially given Priority’s accelerating deposits, enterprise ISV wins adding $10 billion in annual transaction volume, and its new financing facility that supports further partner expansion. For shareholders, the formation of a special committee would be a crucial step toward ensuring that the final outcome—sale or otherwise—is driven by comprehensive market testing rather than the preferences of an insider with majority voting control.

CEO Control & Governance Risk

A major point of contention—and one that amplifies shareholder tension—is Thomas Priore’s substantial control over Priority Technology. With Priore and his affiliates holding roughly 57% of outstanding common stock, he effectively dictates corporate governance outcomes, limiting the influence of minority shareholders unless the board asserts strong independence. This concentration of power raises governance concerns in a take‑private scenario, as the controlling shareholder is also the buyer, creating an inherent conflict of interest. Steamboat Capital’s letter highlights exactly that dynamic, noting that only a special committee can safeguard minority interests. The issue is exacerbated by the timing of the offer, which arrives as Priority reports expanding gross margins, a rising contribution from high‑margin segments, a record increase in deposits under administration, and improved cash generation. These fundamentals may suggest that the company is entering a stronger phase—yet public market valuation remains muted due to small-cap illiquidity, macro-driven volatility, and investor rotation away from fintech. This creates an environment where a controlling shareholder could seek to acquire remaining shares at a discount, prompting scrutiny around fiduciary duties and process integrity. Governance risk is not new for controlled companies, but in Priority’s case, the stakes are heightened by multiple strategic initiatives underway—acquisitions, platform integrations, treasury scaling, ISO/ISV financing—all of which could meaningfully enhance long-term enterprise value. Minority investors may fear that they will not participate in this upside if the company is taken private prematurely. Additionally, the CEO’s central operational role and visibility into pipeline conversions, enterprise partner deployments, and segment‑level contribution trends further complicate perceptions of fairness. If the board does not act decisively, the imbalance of power could lead to reduced transparency, limited negotiation leverage, and decreased confidence among public investors. In this context, governance risk becomes a critical factor influencing both the bidding process and investor expectations.

Non‑Binding Proposal & Deal Execution Uncertainty

Another layer of tension stems from the nature of Priore’s offer itself—it is preliminary, non‑binding, and subject to due diligence, financing, and approval processes that may not materialize as outlined. Non‑binding proposals often serve as exploratory feelers, not firm commitments, and they carry significant execution risk, particularly in controlled-company transactions where conflicts of interest must be navigated carefully. The absence of a binding financing package or finalized terms means shareholders have limited clarity on deal certainty, timeline, or the ultimate price. Meanwhile, Priority continues to execute operationally: Q3 results included 6% revenue growth, 10% adjusted gross profit growth, and 6% adjusted EBITDA growth, while adjusted EPS rose 56% to $0.28. The company also paid down $15 million of debt after quarter‑end, refinanced its term loan at lower rates, and continues deleveraging efforts while maintaining $157 million in liquidity. These developments introduce uncertainty around whether the CEO’s initial price range accurately reflects Priority’s trajectory by the time any transaction would be consummated. If the company posts stronger‑than‑expected Q4 numbers, converts more enterprise pipeline volume, or benefits from easing consumer spending headwinds, the intrinsic value could shift higher—potentially prompting renegotiation or competing bids. Non‑binding proposals also require extensive legal and fairness review, which could extend timelines and raise the probability that no deal is reached. Meanwhile, any disclosure gaps, shifts in consumer spending in Merchant Solutions, or volatility in interest rates affecting Treasury Solutions could alter the financial landscape mid‑process. Until the board forms a special committee and obtains independent valuations, the uncertainty associated with the CEO’s proposal remains a major wildcard for investors attempting to forecast next steps.

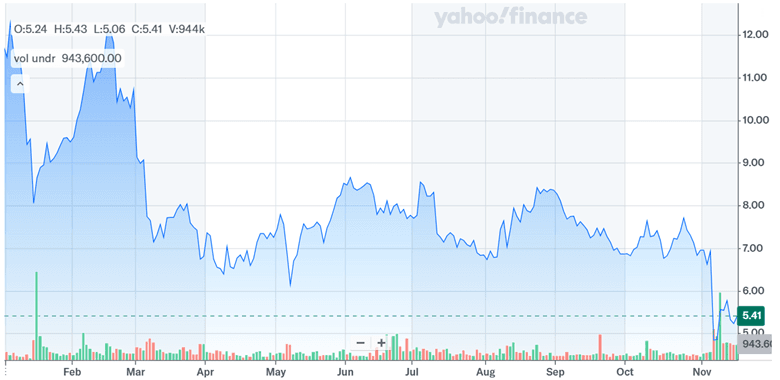

Final Thoughts

Source: Yahoo Finance

Priority Technology is definitely a tricky spot and its stock has been sliding since the beginning of November. As for how the company stacks up against others, its valuation numbers—like 1.50x revenue and 7.26x EBITDA—look kind of low compared to similar companies, but that’s not the whole story. Whether or not those numbers stay that way depends on what the board decides to do next, and whether they open the door to other potential buyers. For now, it is a classic case of a company at a crossroads—with plenty of risk, but also room for things to turn out better if the process is handled fairly.