Sprout Social’s (NASDAQ:SPT) stock caught some fresh attention recently, and not for the usual reasons. On November 17, a new round of takeover rumors hit the wires, with chatter suggesting that Adobe might be interested in scooping up the small-cap social media software company. Traders pointed to a Betaville “uncooked” alert, and while nothing official came out of it, the buzz was enough to turn heads. And it’s not just the chatter—Sprout has been showing some solid progress lately. The company just posted a strong quarter with 13% revenue growth and record profit margins. It is also making waves in the AI space and continuing to grow its big-name client base. Put it all together, and it’s no wonder folks are wondering if a bigger player like Adobe might want in. So what does all this mean for Sprout’s future? Let’s take a closer look.

Strategic Fit With A Larger Platform

When you look at the broader software landscape, Sprout Social’s platform fits neatly into the gap between content creation and customer engagement—an area where large tech companies continue to invest heavily. For Adobe in particular, adding a social media management layer would round out its marketing and creative ecosystem, which powers everything from content creation to customer analytics. Sprout already integrates with Adobe Express, and many of the workflows that marketing teams run through Sprout sit upstream or downstream from Adobe tools. This alone makes the pairing feel logical. Beyond workflow alignment, Sprout has something else large platforms increasingly want: access to real-time social data. Because social networks tightly control who can touch their data, partnerships and licensing agreements matter—and Sprout has deep relationships with major networks including TikTok, Reddit, Bluesky, Snapchat, Instagram, and LinkedIn. Integrating that kind of access with Adobe’s suite could help Adobe strengthen its marketing cloud without building these relationships from scratch. Sprout’s newly announced AI capabilities also play into this dynamic. Its agentic system for spotting trends, analyzing sentiment, and recommending actions draws directly from social data—something Adobe’s customers could benefit from as marketing becomes more real-time and insight-driven. On top of that, Sprout’s enterprise segment is growing rapidly, with nearly 2,000 customers paying over $50,000 per year. These types of accounts line up with Adobe’s core customer base and could open up cross-selling opportunities. Add in the fact that Sprout is still a small-cap, making it more digestible from a balance-sheet perspective, and it becomes clear why analysts see strategic fit as a main driver behind the M&A chatter.

Renewed Takeover Chatter Supports The Stock

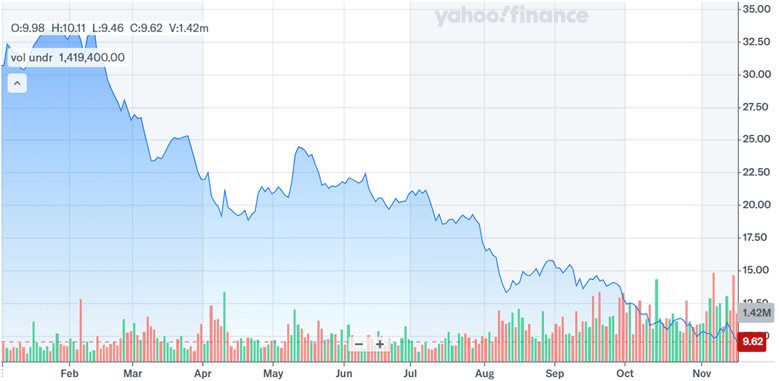

The market’s reaction to the latest takeover rumor wasn’t surprising. Small-cap tech names often experience quick swings on M&A headlines, especially when valuations have compressed as sharply as Sprout’s have. On November 17, the stock pared earlier losses after traders circulated the Betaville alert pointing to Adobe as a potential buyer. Even though the rumor wasn’t confirmed, the idea alone was enough to steady the stock—and that has a lot to do with Sprout’s current valuation. The company is trading at just 1.21x LTM EV/Revenue and 1.28x LTM P/S, far below historical software deal multiples that often land between 5x and 8x revenue. With valuation levels this low, the stock becomes more sensitive to acquisition headlines because investors naturally start asking whether the company looks “too cheap” to ignore. At the same time, Sprout’s fundamentals have been improving. Q3 revenue grew 13%, current remaining performance obligations rose 17%, and the company posted a record 11.9% non-GAAP operating margin. Enterprise deals were strong, including several $1 million-plus wins, and NewsWhip is already boosting deal sizes and pipeline growth. When you pair financial progress with a deeply discounted valuation, it’s easier for investors to imagine strategic buyers taking a closer look. So while the rumor itself may not mean a deal is imminent, it does reinforce what the numbers are already showing: Sprout is reaching a point where its public market valuation and private market value seem out of sync. That gap—real or perceived—can fuel speculation in a stock like this.

Stock Stabilization After Early Losses

The way Sprout’s stock traded on the day of the rumor also tells us something important. Even though shares dipped early, the rebound that followed suggests that investors were willing to look past short-term volatility and instead focus on Sprout’s improving business fundamentals. This is especially noteworthy in a market that has been tough on small-cap software names. One reason Sprout stabilized is that the company’s Q3 call painted a clearer picture of its long-term trajectory. Enterprise demand remains healthy, with large deal momentum at record levels outside the fourth quarter—traditionally the company’s strongest period. Sprout added notable clients such as Bentley Motors, Valvoline, Becton Dickinson, and NYU, and it reported strong adoption of high-value modules like Influencer Marketing, Premium Analytics, Customer Care, and the newly added NewsWhip intelligence tools. Another factor helping sentiment is Sprout’s AI roadmap. The company is rolling out a proprietary AI agent designed to interpret social data, identify risks, detect emerging trends, and recommend actions in real time. This type of product direction taps directly into what many brands are now asking for: faster insights and more automation. Investors may also be giving weight to Sprout’s ongoing shift to multi‑year enterprise deals and rising retention rates, which provide more visibility and stability in the revenue stream. Add in a growing free cash flow profile—80% growth on a trailing 12-month basis—and it's easy to understand why the stock didn’t stay down for long. While rumors played a part in the rebound, the underlying fundamentals helped keep the stock from sliding further.

Rumor-Driven, No Confirmed Bid

Even with the stock’s quick recovery, it’s important to keep things grounded. As of now, no official party—Adobe or otherwise—has confirmed any takeover talks. Betaville alerts often spark chatter, but they don’t necessarily reflect active negotiations. Until a company confirms strategic interest or discloses discussions, the situation remains speculative. That’s especially true for a business like Sprout, where the operational story is still evolving. The company is making progress, but it also has challenges, including ongoing pressure in the SMB and agency segments, which management has acknowledged openly. This part of the business sees lower retention and more volatility, and it has been a drag on overall growth rates even as enterprise performance strengthens. Potential buyers would likely weigh this two-track business dynamic before making a move. Another area of uncertainty is the broader M&A environment. Large acquirers like Adobe are being more selective amid regulatory scrutiny, shifting budgets, and longer payback timelines on integrations. And despite Sprout’s lower valuation, takeover interest doesn’t automatically translate to a formal offer. Sprout has not indicated publicly that it’s exploring alternatives, and nothing in its recent filings or earnings commentary hints at M&A as a near-term priority. That means investors should treat the current chatter as exactly that—chatter. It may reflect Sprout’s strategic appeal, but without concrete steps or disclosures, the path forward remains uncertain.

Final Thoughts

Source: Yahoo Finance

So, what’s really going on with Sprout Social? The stock has been on the downslide over the past years but bounced slightly after those Adobe takeover rumors which shows there is definitely some excitement in the air. Right now, it’s trading at just 1.21x its last twelve months’ revenue—way lower than what similar software companies usually go for. That could make Sprout an appealing target. And honestly, it makes sense. Sprout’s been putting up solid numbers lately—growing revenue, landing big enterprise clients, and rolling out new AI tools that could be a game-changer for how brands use social media. But before we all get ahead of ourselves, let’s not forget: this is still just a rumor. Nobody has confirmed anything, and Sprout hasn’t said it’s looking to sell. But whether or not a deal happens, the company’s future still depends on how well it keeps growing and managing its business. For now, it’s worth keeping an eye on—just don’t bank on the rumor alone.